Umami v2 GLP Vaults — Initial Backtesting Results and Analysis

Over the past few months, Umami has been hard at work developing an algorithmic hedging strategy for Umami’s upcoming v2 GLP Vaults.

In designing the Vaults, the team has aspired to create a trustless DeFi strategy that generates Delta-minimized returns on assets including USDC, BTC and ETH. To that end, Umami built a detailed simulation of the finalized Vault strategy and backtested it against approximately 8 months of real-world market data.

In today’s report, the team is proud to share the initial results and findings from its simulation and backtests. Umami looks forward to sharing additional data and analysis as it gets closer to launching the Vaults.

Highlights

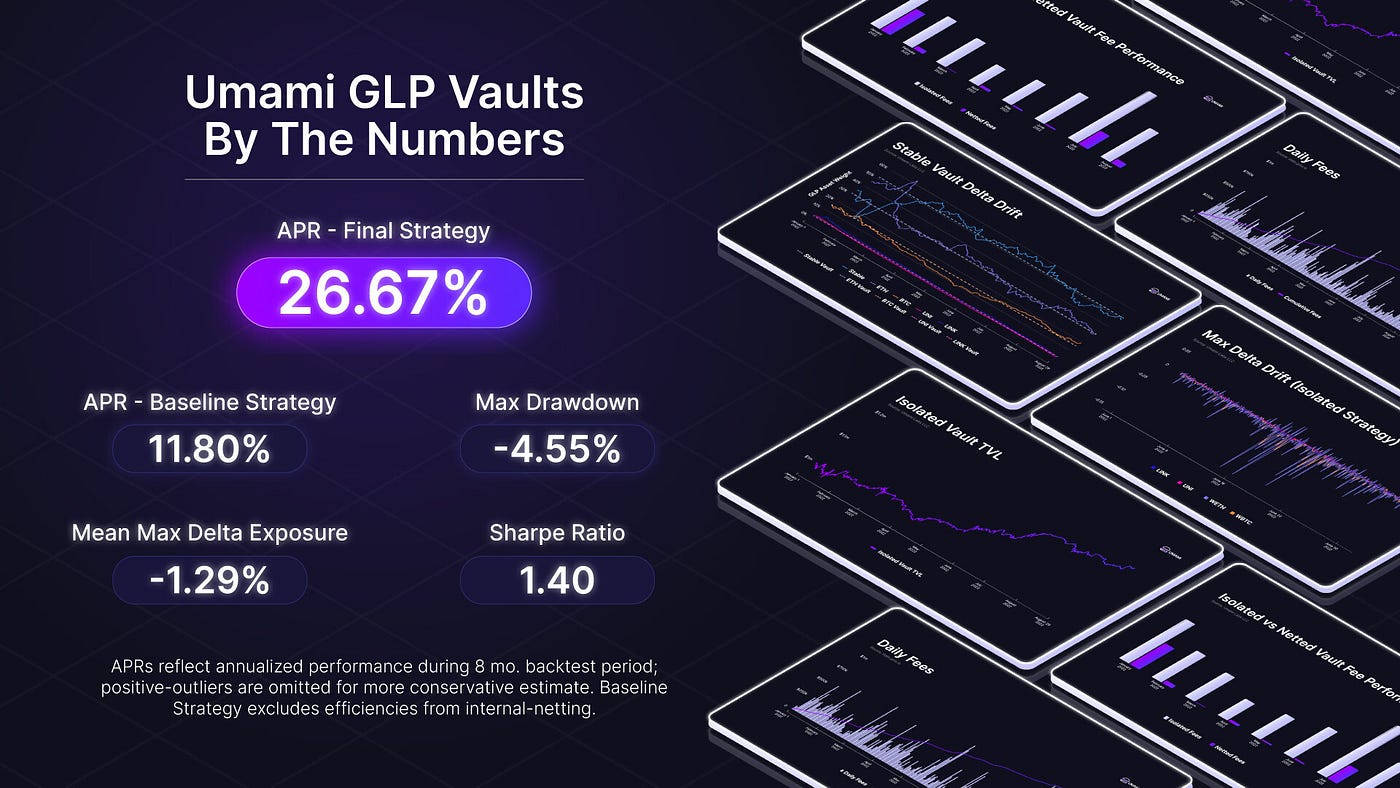

- Annualized Returns, Final Strategy: 26.67%

- Annualized Returns, Baseline Strategy: 11.8%

- Worst-Case Drawdown: -4.55% (incl. Trader PnL)

- Mean Max Delta Exposure: -1.29% (Std Dev. 2.10%)

- Sharpe Ratio: 1.4

Notes

- Annualized Returns (Final Strategy and Baseline Strategy) are based on backtests covering 8 months of real-world data from Jan.-Aug. 2022. Both figures exclude positive-outlier data from 2 months of highly-favorable Trader PnL in May and June for a more conservative estimate.

- Annualized Returns, Final Strategy includes capital efficiencies from internal netting and assumes Vault TVL balances that approximately align with asset allocations in GLP.

- Annualized Returns, Baseline Strategy reflects the performance of a hypothetical standalone USDC Vault and completely excludes efficiencies from internal netting.

- Worst-Case Drawdown is based on Max Peak-to-Trough during Jan.-Aug. 2022. It includes GLP losses from unfavorable Trader PnL and assumes zero capital efficiencies from internal netting.

- Max Delta Exposure represents the % of the Vaults’ TVL that is exposed to market-risk from price changes in GLP’s volatile assets. For example, with a Delta exposure of 1.29%, a 1% change in the price of GLP’s volatile assets would impact Vault TVL by 0.0129% (1% * 1.29%).

- Sharpe Ratio is calculated using the standard formula. It is based on the performance of the Baseline Strategy and assumes a risk-free rate of zero.

Overview

Umami’s GLP Vaults are a suite of trustless, non-custodial DeFi strategies designed to generate exceptional risk-adjusted returns on USDC, BTC and ETH. They also include small TVL allocations for UNI and LINK deposits.

The Vaults provide liquidity to GMX, a decentralized perpetuals exchange on Arbitrum, and collect Yield from GLP, GMX’s Liquidity Provider (LP) token. The GLP asset receives 70% of GMX’s fee revenue. It also functions as a counterparty to margin traders on GMX and benefits from trader-losses.

Meanwhile, the Vaults hedge against unwanted market-Delta exposure using a capital efficient internal netting strategy, which reallocates Delta among the Vaults to minimize hedging costs. The Vaults also hedge externally on GMX. Hedges are algorithmically rebalanced at regular intervals.

In backtests, Umami’s GLP Vaults generated annualized returns of approximately 26.67% while maintaining a Mean maximum Delta exposure of approximately -1.29%. Internal netting reduced hedging costs for the Vault strategy by 65% to 95%. During the backtesting period, the Vaults benefited significantly from net-losses by GMX margin traders.

Purpose and Methodology

The purpose of Umami’s simulation and backtesting analysis was to optimize the GLP Vaults’ hedging strategy by stress-testing it against all available historic data as well as a variety of hypothetical market scenarios and edge-cases.

To create the simulation, the Umami team pulled all available GMX and GLP data directly from the blockchain — with 1-second-interval time-granularity — and replicated all of the GMX and Umami Vault smart contracts in Python.

The result was a comprehensive simulation that dynamically modeled the performance of GMX, GLP and Umami’s v2 Vaults. The simulation accounted for all historic data on prices, allocations, fees and yield for assets in the GMX/GLP contracts. It also carefully accounted for the impact of feedback loops between Umami’s Vaults and GMX/GLP.

Umami’s GLP Vault simulation has been an invaluable tool and has provided deep insights into the challenges and payoffs of potential strategies built on top of GMX.

Results and Analysis

GLP Performance

GLP is a tokenized “receipt” for GMX’s Liquidity Providers (LPs). It represents a claim on the basket of assets in GMX’s Liquidity Pool, which is comprised of stablecoins, BTC and ETH, as well as small allocations of LINK and UNI. GLP’s liquidity enables leveraged trading and swaps on GMX.

GMX incentivizes LPs by paying 70% of its platform-fee revenue to GLP holders. The GLP Liquidity Pool also acts as a counterparty for margin traders on GMX. When GMX traders “lose,” they forfeit their collateral to GLP. Conversely, “winning” traders collect payouts at GLP’s expense. Historically, GLP has benefited significantly from net losses by traders.

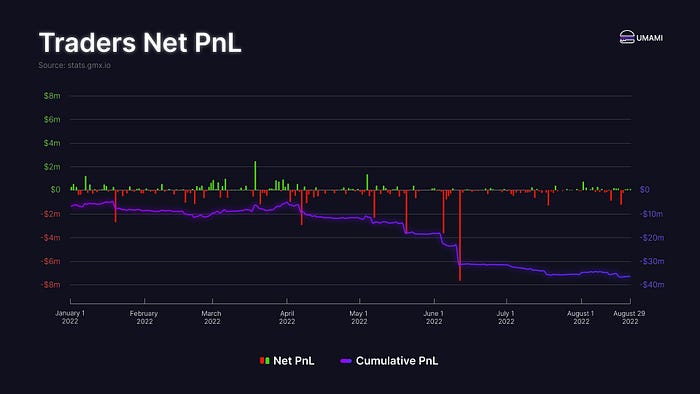

GMX’s Stats page provides detailed data on protocol revenues from Platform Fees and Net Trader Profit-and-Loss (PnL). During the 8 month backtesting period, GMX traders suffered heavy net-losses and GLP gained approximately $30 million from Cumulative Net Trader PnL. Daily fees were relatively volatile but averaged around $200k/day.

Hedging Considerations

As the figures above illustrate, GLP is a very attractive asset. However, it is also highly dynamic and poses unique challenges for any strategy attempting to consistently hedge GLP’s exposure to market Delta. The asset allocations in the GLP Liquidity Pool can change rapidly and unpredictably based on factors such as trader activity and GLP mints/burns.

Umami’s simulation demonstrated that hedging strategies that ignore GLP’s highly dynamic asset allocations perform very poorly. Exposure to market Delta and sharply changing asset prices can quickly wipe out gains.

The team recognized early on that dynamic external hedging would be critical for any successful strategy. Moreover, the appropriate hedging instrument needed to be deeply liquid, highly capital-efficient and amenable to dynamic position adjustments. GMX’s leveraged perpetuals exchange emerged as the ideal solution.

However, continually rebalancing hedges to adapt to GLP’s dynamic asset weightings can become extremely costly if improperly managed. Hedging on GMX incurs fees for minting and burning of GLP, opening and closing positions, and funding open interest. Therefore, it was crucial for Umami to develop a nuanced rebalancing algorithm that neutralized Delta exposure while also minimizing hedging costs. Early simulations demonstrated that the frequency of hedging rebalances is an especially important determinant of strategy performance.

Baseline Strategy Performance

Umami’s first step was to develop a Baseline Strategy for hedging a standalone USDC Vault. The Baseline Strategy does not factor in any capital efficiencies from internal netting among all of the Vaults. It assumes all hedging is done externally at GMX, resulting in much higher hedging costs.

Such a scenario is highly unlikely. However, in developing a viable Baseline Strategy, Umami has helped ensure its Vaults will perform strongly even with imbalanced TVL.

It is important to note that the Baseline Strategy only applies to a standalone USDC Vault. Hedging costs would be significantly higher in standalone Vaults for assets with smaller allocations in GLP, such as LINK.

Umami backtested the Baseline Strategy against 8 months of real world data from January to August, 2022. The strategy performed well, generating a return of 18.55% for the 8 month period and an annualized return of 27.8%.

Its performance benefited significantly from counterparty exposure to margin traders on GMX. During the 8 month backtesting period, GLP gained a Net $29.7m from Trader PnL. More than half of GLP’s net gains occurred in May and June. During both of those months, extreme crypto market drawdowns contributed to elevated trader liquidations on GMX.

For a more conservative assessment of performance, Umami Labs decided to omit data from May and June from its final annualized return figures. Excluding those positive outliers, the Baseline Strategy generated annualized returns of 11.8%.

Even excluding the two outlier months, the Baseline Strategy benefitted significantly from Trader PnL. However, even if upside from Trader PnL is excluded completely, the strategy’s annualized returns remain positive. The Baseline Strategy’s annualized APR from platform fees alone was 3.3%.

It is important to note that GLP’s exposure to counterparty risk was not exclusively beneficial. During the 8 month backtesting period, the Baseline Strategy saw a Max Drawdown of 4.55% from peak to trough, primarily due to a period of unfavorable Net PnL.

However, given the overall positive net-impact of GLP’s counterparty exposure, the main objective of the Baseline Strategy has been to minimize exposure to volatile asset Delta in GLP.

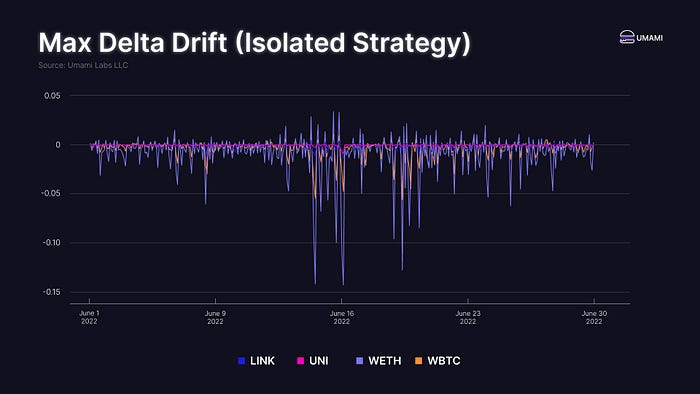

In backtesting, Umami’s hedging algorithm offset GLP’s Delta nearly perfectly at the start of each rebalancing period. Between rebalances, changes in the spot prices and allocations of GLP’s volatile assets caused the Vault’s Delta-exposure to drift. On average, the maximum Delta-exposure between rebalances was -1.29%, with a Standard Deviation of 2.10%.

The maximum Delta-exposure represents the percentage of TVL in Umami’s Vault that is exposed to market-risk from changing spot prices on GLP’s volatile assets. For example, a 1.5% Delta-exposure indicates that only 1.5% of Vault TVL would be effected by changing prices of assets in GLP. Therefore, a 1% change in spot price across all of GLP’s volatile assets would result in a 0.015% loss of value in Umami’s Vaults (1.5%*1%).

The Vault’s extremely low Mean maximum Delta exposure suggests that Umami has created a highly successful Delta-minimized Yield strategy.

Annualized Returns, Baseline Strategy: 11.8%

Max Drawdown: -4.55%

Final Strategy Performance

With the Baseline Strategy complete, the Umami team progressed to its Final Strategy, which incorporates capital efficiencies from internal netting.

Umami’s internal netting strategy is an advanced Delta-optimization algorithm that allocates Delta from each of the constituent assets in GLP to the corresponding Umami GLP Vault. Any remaining unwanted exposure is hedged externally using third party protocols. Internal netting enables Umami’s Vaults to offset market delta in GLP with extreme precision. At the same time, it greatly reduces reliance on costly external hedges and improves overall capital efficiency.

One of the most important variables in the success of Umami’s internal netting strategy is the TVL balance across its various GLP Vaults. The more closely the balance aligns with the real-time weighting of GLP, the lower the overall cost of hedging for the strategy.

During backtesting, Umami was required to make assumptions about the balance of Vault TVL, which are illustrated in the above chart (Stable Vault Delta Drift). The chart tracks fluctuations in the distribution of GLP assets over the 8 month backtesting period.

The data affirms that the more closely TVL in Umami’s Vaults aligns with GLP’s asset allocations, the better the Vaults perform. Umami’s rebalancing algorithm includes strategies for aligning Vault TVL with GLP asset distribution to maximize performance.

Umami’s Final Strategy includes 5 GLP Vaults (USDC, BTC, ETH, UNI and LINK) that internally net Delta exposure to minimize hedging costs and maximize TVL allocated to GLP. On average, the internal netting strategy reduced hedging costs by 65%-95%, depending on the distribution of Vault TVL and GLP composition. The strategy also increased the proportion of Vault TVL deployed in GLP by 11%.

As a result, overall returns for the Final Strategy during the 8 month testing period were extremely strong. The Vaults returned 26.35% for the period or 39.52% on an annualized basis.

Once again, Umami’s final figure for annualized returns conservatively omits the positive outlier months May and June. The result was still an exceptional annualized return of 26.67%.

Crucially, the Final Strategy produced highly attractive returns even after omitting gains from Net Trader PnL entirely. Based on platform fees alone, the Final Strategy generated annualized returns of 16.2%.

Annualized Returns, Final Strategy: 26.67%

The Next Steps

Suffice it to say that the initial backtesting results have been extremely promising. With the finalized Vault Strategy in place, Umami Labs is now focusing on completing the Vaults’ smart contract code ahead of a planned audit later this month.

That said, the team will continue to analyze the backtesting results in detail with eye for further improvements to Umami’s Vault strategy, including:

- Optimizing strategy hyper parameters for increased performance.

- Testing the effects of hedging GLP’s counterparty exposure.

- Ensuring protection in edge cases, including stress-testing extremely dramatic changes in GLP allocations, prices or TVL.

- Developing solutions for adapting to dynamic Open Interest caps on GMX.

- Exploring the impacts of different fee structures.

Remember, today’s preliminary report covers only a small fraction of the data generated from Umami’s backtests. Moreover, the team is continuing to pull more real-world data to backtest the strategy over an even longer period.

For a richer trove of data and additional analysis, stay tuned for Umami’s Whitepaper, which will be published shortly before Vault launch.